QIMA 2024 Q3 Barometer

Q3 2024 BAROMETER: Halfway into 2024, Global Sourcing is on a “See-Saw” Trend

So far this year, global procurement volumes have been trending upwards, reflecting increased consumer optimism in parts of the West and efforts to restock inventories after a subdued 2023. Meanwhile, on the supply side, many manufacturing hubs across Asia are experiencing a “see-saw” effect, with some sourcing markets, such as Vietnam, Bangladesh and India, rebounding after a lackluster 2023, while some of last year’s leading markets are showing a slowdown.

China stands out as an exception to this “see-saw” trend, successfully building on last year’s recovery – but even the manufacturing giant is not immune to the uncertainty that comes with geopolitical developments, such as Russia’s ongoing war in Ukraine and the upcoming US presidential election.

This barometer report, drawing on QIMA’s extensive data on product inspections and factory audits, delves into the trends that have been shaping the supply chain landscape throughout the first half of 2024.

China’s Manufacturing Remains a Cornerstone of Global Supply Chains

After starting 2024 with a bang, China sourcing has maintained momentum throughout the second quarter, with demand for the “world’s factory” high in the West as well as the emerging markets.

QIMA data on inspection and audit demand among European companies underscores China’s importance in their supply chains. Inspections and audits ordered by German businesses expanded by +27% year-on-year in Q2 ’24; meanwhile, just outside the EU, the UK also showed strong demand for China sourcing with a +32% YoY growth in inspections and audits.

Meanwhile, US-based buyers showed a more measured approach towards China sourcing amid the ongoing efforts to “de-risk” supply chains in favor of “friend-shoring”. Nevertheless, demand for inspections and audits in China from American brands and retailers rose by +13% YoY in Q2 2024. This growth spanned a variety of consumer goods categories, including apparel, toys, homewares, and electronics. While these figures might partly represent a “normalization” effect as consumer sentiment improves after a sluggish 2023, they underscore China’s significance as a partner for Western supply chains. This is further evidenced by the uptick of China’s relative share in the supplier portfolios of European and American brands compared to 2023.

China’s trade with emerging economies keeps growing by leaps and bounds in the meantime: QIMA data shows an ongoing surge in demand for China inspections and audits from clients across Latin and South America, as well as elsewhere in Asia. Mexican businesses in particular are eager to do business with Chinese suppliers, both in the context of US nearshoring and to supply Mexico’s own booming consumer market.

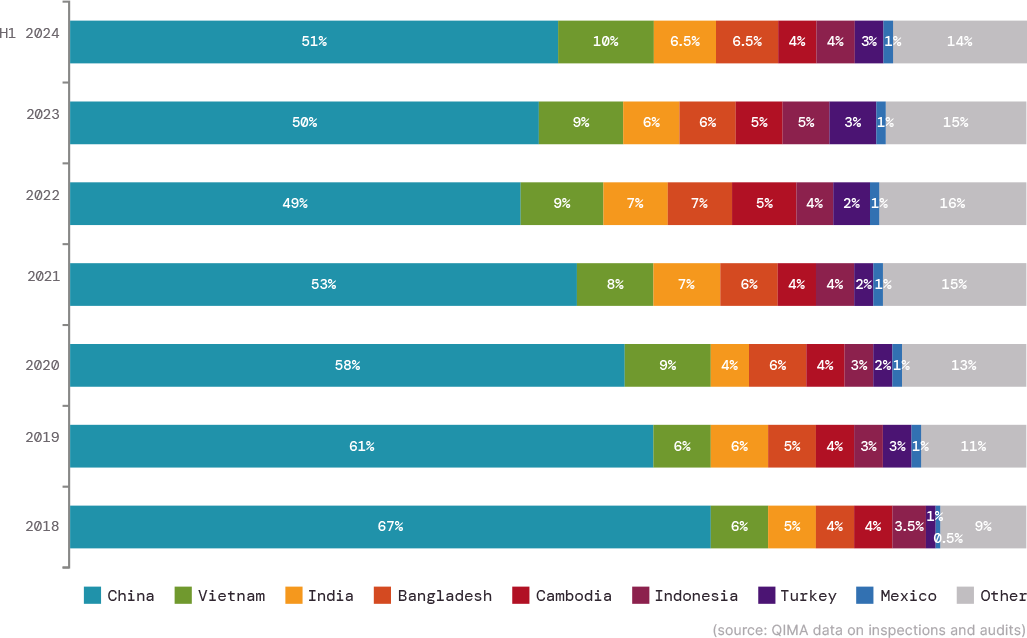

Fig. C1. US and EU top sourcing markets by relative share

Mexico: More Than Just the Factory Floor for US Nearshoring

While Mexico has been making headlines as a promising supplier partner for US-based brands keen to buy closer to home, its growth as a consumer market should not be overlooked.

QIMA data on inspections and audits shows that Mexico’s overseas procurement has been booming so far in 2024, with China as the top supplier partner (+69% YoY spike in inspection and audit demand in H1 ‘24), and trade with Vietnam and Cambodia growing as well. While US nearshoring initiatives undoubtedly contribute to this trend, a notable portion of Mexico’s purchasing volumes likely caters to its own domestic market – especially given the evidence that US nearshoring in Mexico may not be expanding as rapidly as anticipated.

Indeed, despite the high interest in nearshoring displayed by American businesses in QIMA’s 2024 Sourcing Survey, data on actual sourcing volumes shows sluggish demand for inspections and audits in Mexico from US-based buyers in H1 2024. Constraints of Mexico’s energy grid and high levels of bureaucracy are commonly cited among factors currently slowing down the growth of nearshoring projects.

Fig. M1. Buyers planning to use nearshoring and reshoring as part of their 2024 supply chain strategy

Europe’s Nearshoring Efforts Outpace the US, with Turkey a Key Supplier Partner

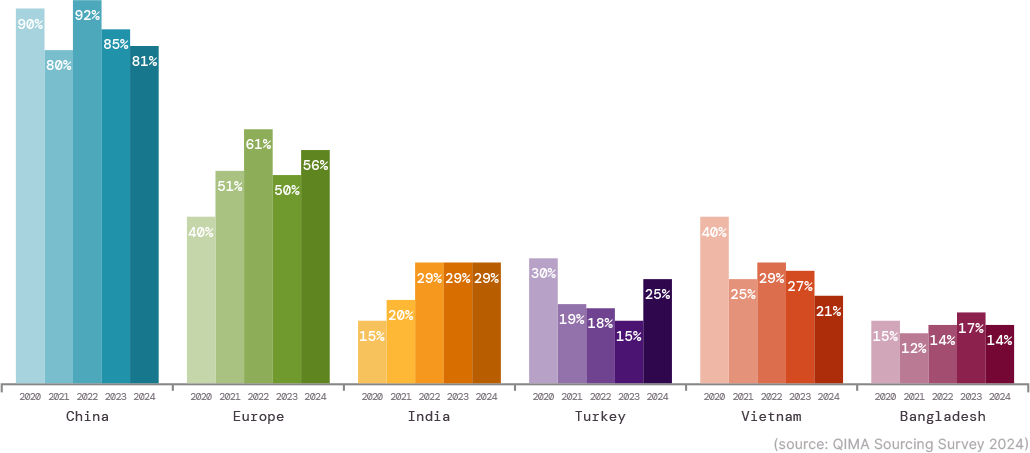

While US nearshoring faces some stumbling blocks, Europe’s efforts to shorten supply chains have been more successful, QIMA data suggests. Over the past two years, demand for inspections and audits from European buyers has been on a steady upward trajectory in Turkey (+27% YoY in Q2 ‘24), which a quarter of EU-based businesses identified as one of their top three sourcing partners in QIMA’s 2024 sourcing survey.

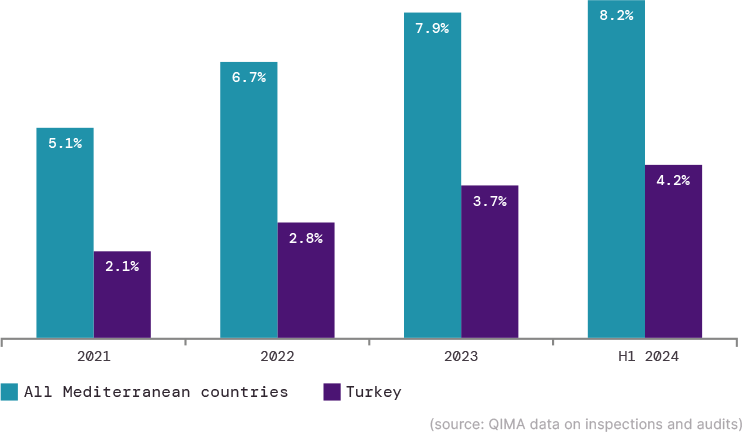

Furthermore, demand for inspections and audits also expanded in Egypt, Tunisia, Morocco, and other supplier markets around the Mediterranean, which now accounts for over 8% of European buyers’ procurement globally. The diverse selection of supplier hubs in the region and the effective utilization of well-established trade links may account for the fact that European brands and retailers have been more active in executing their nearshoring strategies compared to their American counterparts.

Fig. T1. Countries and regions named by EU-based businesses as top three sourcing partners

Fig. T2. Relative share of the Mediterranean countries and Turkey in sourcing portfolio of EU-based buyers

While ESG Regulations Strengthen, Child Labor and Worker Safety Issues Remain Rampant in Global Supply Chains

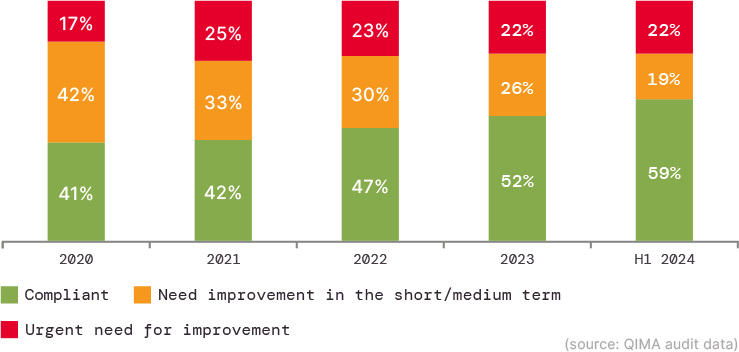

The final adoption of the EU Corporate Sustainability Due Diligence Directive (CSDDD) in May has further elevated the standards for ethical compliance across global supply chains. QIMA data on factory audits, meanwhile, suggests that years of incremental progress in this area may finally be bearing fruit in China. Among factories inspected in China by QIMA ethical audits in H1 2024, 59% received a “green” ranking for compliance – a five-year high. Notably, the percentage of “red” (critically non-compliant) facilities has remained stable over several years, suggesting that, despite the progress being made, a certain share of factories tends to resist improvement,

while the rest are successfully implementing corrective action plans, working towards full compliance. Factory audits likely play a significant role in this, with QIMA data on audit volumes showing a +62% increase in demand for ethical audits among Chinese businesses in H1 2024.

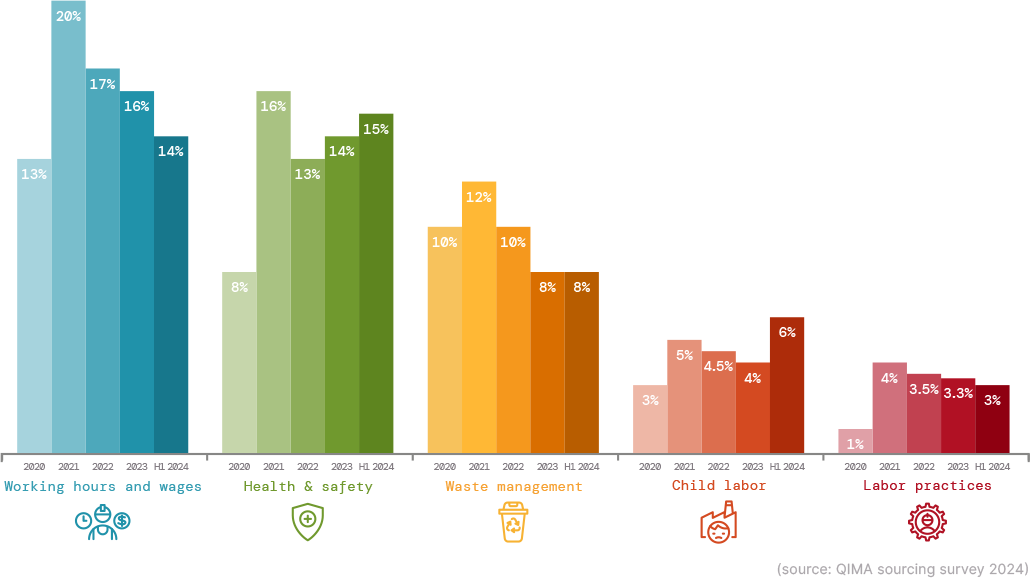

Despite these encouraging developments, there is no room for complacency. A broader analysis of QIMA’s audit results shows that the frequency of violations related to child and young labor has been on the rise globally over the past several years, with critical non-compliances in this category discovered in 6% of ethical audits conducted by QIMA in H1 2024. Worker safety also remains a pressing concern: 15% of QIMA’s ethical audits identified critical Health & Safety violations in H1 2024, while dedicated structural audits determined that over three-quarters of factories were in need of remediation for issues of structural, fire or electrical safety.

These findings make clear that despite the notable progress in ethical compliance, continued vigilance and ongoing corrective action are essential to address persistent ESG challenges in global supply chains.

Fig. E1. Evolution of factory ethical compliance rankings in China, 2020-2024

Fig. E2. Percentage of audits discovering critical violations in given categories (globally)

Press Contact

Email: press@qima.com